Susan Dworak (sdworak@realidentities.com) is a legal compliance and identity expert based in Silicon Valley, California, USA. Teri Quimby (teri@teriquimby.com) is an attorney, speaker, author, consultant, and former state regulator in Lansing, Michigan, USA.

Government often finds itself in the uncomfortable situation of applying old regulations to new ideas; it’s a regulator’s worst nightmare. Legal and regulatory umbrellas need to be flexible enough to expand with the passage of time, yet definitive enough to endure history in the making. For example, a decade ago the ideas of social media and apps were different than today. The idea of ordering a cup of coffee using an app, paying for it, and picking the product off the counter with your name on it—without talking to a single human being—seemed unimaginable. Enter disruptive blockchain-based solutions, which may initially sound like something from a sci-fi movie. While the idea of an immutable, irreversible distributed ledger technology may disrupt the way we do business in many sectors in society, it definitely does so with increased attention from and scrutiny by government officials. The key is to implement regulations based on enduring legal principles that can be applied in the future even as the underlying technology changes. We don’t know what future technology brings, so applicability should include some level of discretionary authority. Flexibility and agility provide authority even when the rate of technology disruption appears to make promulgation of a regulatory framework tantamount to hitting a moving target.

The ABCs of blockchain

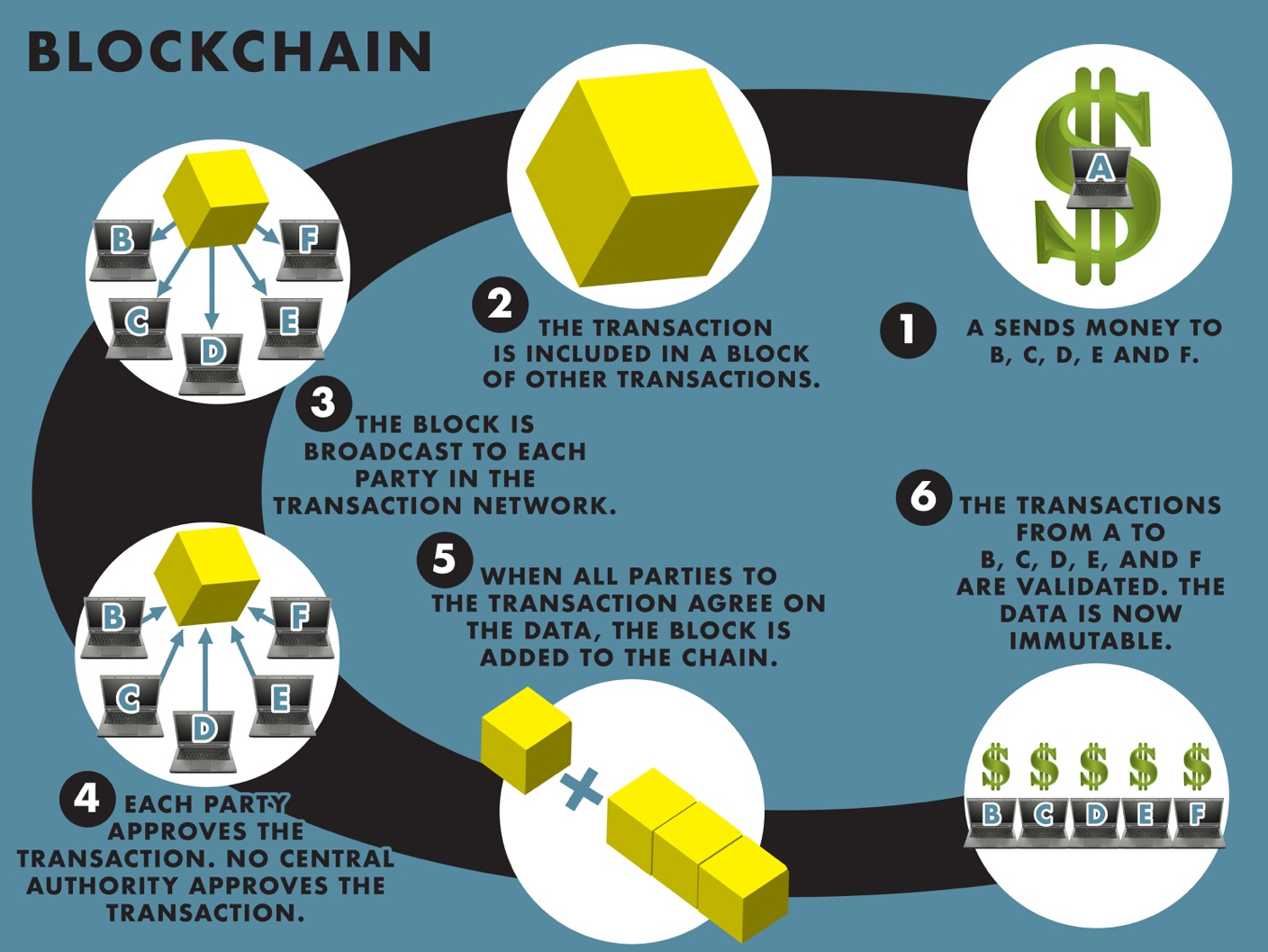

Blockchain is an online open ledger that can be used by multiple parties to record nearly any kind of transaction or to store data that cannot be changed. The ledger consists of a growing list (chain) of records (blocks) that are linked together (blockchain). Each block has a “cryptographic hash” of its contents and the hash of the previous block. The hash links the blocks together in a chain. Each block also has a permanent time stamp. In this way, any transaction or data stored in the block is secure and cannot be changed—it is immutable (Figure 1). The ledger is secure and resistant to modification—if contents of any block are altered after validation by the other parties to the transaction involved, the hash will not match. Since the data in the block is visible to all parties, it is a trivial calculation to verify the hash for any block in the chain.

Blockchain, therefore, is a process of securing data. The records are stored in a peer-to-peer network, such as a cell phone or computer (nodes). Since every member of the network has a copy of the data, rather than one single source, this is referred to as a distributed ledger technology. Because the parties to the network are mutually agreeing on each block of data, blockchain operates without the need for a traditional central authority such as a bank or government agency.